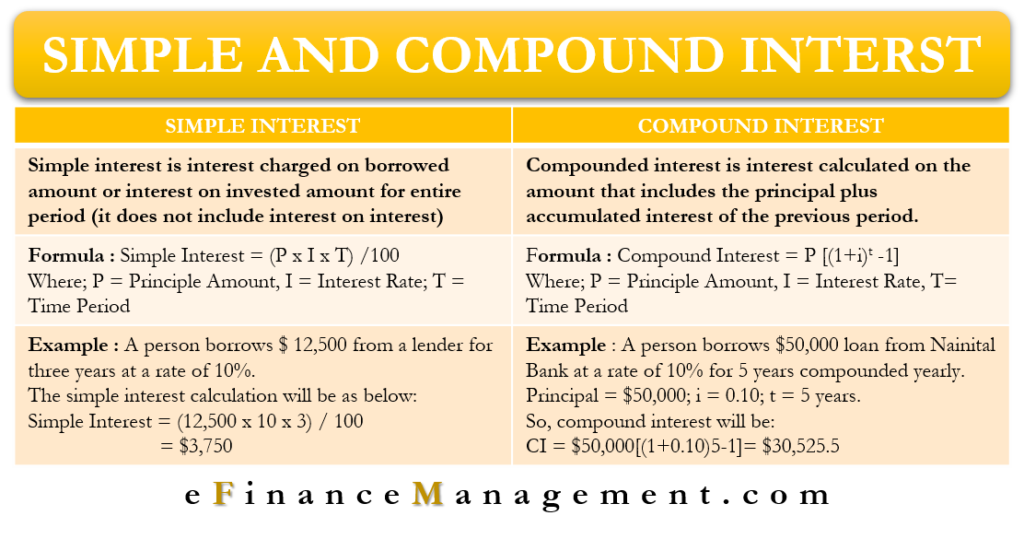

Definition of Simple Interest

Simple interest is a type of interest that is calculated only on the principal amount of a loan or investment. This means that the interest remains constant throughout the loan term, as it is not applied to the accumulated interest like compound interest. In essence, simple interest is a straightforward method of calculating the amount of interest accrued over a specific period of time based solely on the initial amount borrowed or invested. It is commonly used for short-term loans or investments where the interest is calculated as a percentage of the principal amount.

Definition of Compound Interest

Compound interest is a concept in finance that involves not only earning interest on the initial principal amount but also on the accumulated interest from previous periods. In simpler terms, it is interest that is calculated on both the principal amount and any interest that has already been earned. This means that as time goes on, the total amount of interest earned grows exponentially, leading to a significant increase in the overall value of the investment.

The formula for compound interest takes into account the compounding periods, the interest rate, and the initial principal amount. By reinvesting the earned interest back into the principal, the amount of interest earned in each subsequent period increases. This compounding effect can greatly boost the returns on an investment over time, making compound interest a powerful tool for growing wealth steadily.

Compound Interest Calculator can help in understanding the concept of compound interest. It involves earning interest on the initial principal amount and the accumulated interest from previous periods. The formula considers compounding periods, interest rate, and principal amount, leading to exponential growth in investment value over time.

Calculation of Simple Interest

To calculate simple interest, you need to know three key components: the principal amount borrowed or invested, the interest rate charged or earned, and the time period for which the interest is calculated. The formula to find simple interest is straightforward: Principal amount multiplied by the interest rate multiplied by the time period (in years). For example, if you borrow $1000 at an annual interest rate of 5% for 3 years, the simple interest would be $150 ($1000 * 0.05 * 3 = $150).

Simple interest calculations are often used in scenarios where interest is applied only to the original principal amount without considering any interest that accumulates over time. This method is commonly employed in loans with short terms or investments with fixed returns. Unlike compound interest, which takes into account interest on interest, simple interest offers a more basic approach to understanding how interest accrues on a given sum of money over time. By mastering the calculation of simple interest, individuals can make informed decisions regarding borrowing, lending, or investing money.

Calculation of Compound Interest

Calculating compound interest involves the use of a formula that takes into account both the principal amount and the interest rate. The formula for compound interest is A = P(1 + r/n)^(nt), where A represents the total amount, P is the principal amount, r is the interest rate, n is the number of times interest is compounded per year, and t is the number of years the money is invested for.

To calculate compound interest, one needs to carefully plug in the values of P, r, n, and t into the formula and solve for the total amount. This process ensures that the interest is not only earned on the initial principal but also on the interest that has been added to the principal at each compounding interval. The compounding frequency plays a crucial role in determining the final amount, as more frequent compounding leads to higher overall returns due to the effect of compounding on the interest earned.

Differences in Frequency of Interest Calculation

When it comes to interest calculation, the frequency at which it is calculated plays a significant role. In simple terms, the more frequently interest is calculated, the more interest you will earn. For example, if you have an investment that compounds interest monthly versus annually, you will earn more with the monthly compounding due to the more frequent calculations.

Conversely, if interest is compounded less frequently, such as annually versus quarterly, you will earn less interest over time. This is because with less frequent compounding, your initial investment does not have the opportunity to grow as much as it would with more frequent compounding. Therefore, the frequency of interest calculation is an important factor to consider when evaluating the growth potential of your investments.

FD Calculator is a useful tool for estimating the growth of your investments. Differences in frequency of interest calculation can significantly impact your earnings. More frequent compounding results in higher interest earnings, while less frequent compounding leads to lower overall growth potential.

Effect of Time on Simple Interest

When considering simple interest, the effect of time plays a significant role in determining the total interest earned. The formula for calculating simple interest is straightforward – Principal x Rate x Time – where time refers to the number of periods the principal amount is invested or borrowed for. As time increases, the total interest earned also increases linearly, as long as the principal and interest rate remain constant. This means that the longer the period of time the principal amount is invested or borrowed for, the greater the simple interest accrued.

It is essential to note that unlike compound interest, simple interest does not factor in any interest earned on the interest itself. Therefore, the growth of the investment or debt is constant over time, following a linear trajectory. This makes simple interest easier to calculate and understand, as the interest amount stays the same for each time period it is calculated for. However, this also means that the growth potential of an investment or debt under simple interest is limited compared to compound interest, where interest is calculated on both the principal and accumulated interest.

Effect of Time on Compound Interest

As time passes, compound interest continues to have a profound impact on the growth of an investment. Compounding allows for the reinvestment of both the initial principal amount and the accumulated interest, enabling the total amount to grow at an accelerated rate. The longer the investment remains untouched, the greater the impact of compounding becomes, leading to exponential growth in the value of the investment.

The power of compounding over time is exemplified by the concept of the “time value of money.” This principle acknowledges that a sum of money received in the present is worth more than the same amount received in the future due to its potential earning capacity. With compound interest, the longer the investment horizon, the higher the returns. This highlights the importance of early investment decisions in order to take full advantage of the compounding effect and maximize the growth potential of the investment.

Comparison of Growth Potential

When comparing the growth potential of simple and compound interest, it is essential to understand how each type of interest impacts the overall return on an investment. With simple interest, the interest is calculated only on the principal amount initially invested. This means that the growth potential remains constant over time as the interest is not reinvested or added back to the principal amount.

On the other hand, compound interest allows for exponential growth as the interest is calculated on both the initial principal and any accumulated interest. This compounding effect leads to a higher growth potential over time compared to simple interest. The longer the investment period, the more significant the difference becomes between the growth potential of simple and compound interest, making compound interest a more attractive option for long-term investments.

RD Calculator provides a helpful tool for comparing the growth potential of simple and compound interest. Compound interest offers exponential growth by reinvesting interest earned, resulting in higher returns over time. In contrast, simple interest provides a constant growth potential as interest is not reinvested.

Factors Influencing Interest Rates

Interest rates are primarily influenced by the level of inflation in the economy. When inflation is high, central banks often increase interest rates to curb excessive borrowing and spending, which can further fuel inflation. On the other hand, during periods of low inflation or deflation, central banks may opt to lower interest rates to stimulate economic activity and encourage borrowing and investment.

Another key factor that impacts interest rates is the overall health of the economy. In times of robust economic growth and low unemployment rates, central banks may raise interest rates to prevent an overheating economy and inflationary pressures. Conversely, during economic downturns or recessions, central banks may lower interest rates to stimulate spending and investment, thus aiding in the recovery process.

Trading App Interest rates are primarily influenced by inflation levels. High inflation leads to rate hikes to control spending. Economic health also affects rates, with growth prompting increases and downturns prompting decreases to stimulate economic activity and investment.

Real-life Examples of Simple and Compound Interest

In real-life scenarios, simple interest is commonly used in situations where a fixed interest rate is applied to a principal amount over a set period of time. For instance, when individuals take out personal loans or auto loans, they often encounter simple interest calculations. This straightforward method is favored for its ease of understanding and transparent calculation process.

On the other hand, compound interest is prevalent in investments, savings accounts, and credit cards. With compound interest, not only is the initial principal amount considered, but the accumulated interest is also factored in for subsequent interest calculations. This compounding effect leads to exponential growth of funds over time, which can be advantageous for long-term investments and savings goals.